Dead Capital and Live Debate

What the airport privatization argument gets wrong — and what it cannot bring itself to ask

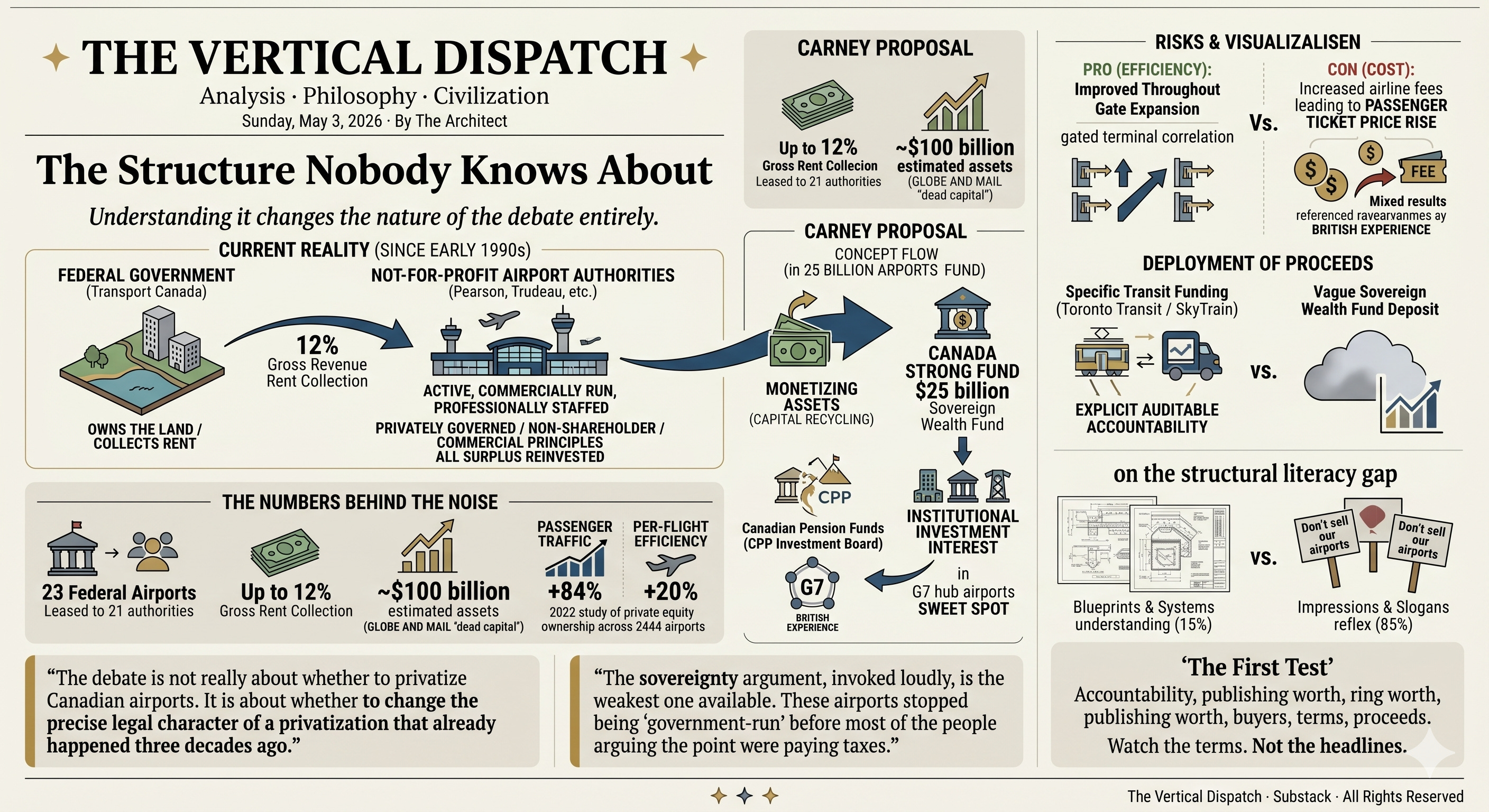

Understanding it changes the nature of the debate entirely.

Not because the concerns are illegitimate. Not because Canadians are wrong to care about what happens to the infrastructure their parents and grandparents built and paid for. But because the argument being made in most quarters — with genuine passion and genuine conviction — is an argument about a reality that no longer exists. And a country that cannot accurately describe what it already has cannot intelligently decide what to do with it.

That is the problem. Not the policy. The literacy.

The Structure Nobody Knows About

Here is the first fact that gets quietly swallowed by every heated opinion on this topic: Canada’s major airports are not run by the federal government. They haven’t been since the early 1990s. Transport Canada owns the land — 23 airports on federal property — but the operations were long ago handed to not-for-profit airport authorities: private corporations, locally governed, not answerable to shareholders, reinvesting their revenues into infrastructure rather than distributing profits.

Pearson. Vancouver. Trudeau. Calgary. Edmonton. Ottawa. These are not government-operated facilities in any meaningful day-to-day sense. They are run by boards, staffed by professionals, and operated on commercial principles — with one critical distinction from a purely private model: no one takes a dividend. The surplus stays in the airport.

This is not an obscure administrative footnote. It is the foundational fact of the entire conversation. And the fact that it is routinely omitted — by commentators, by politicians, by people who consider themselves informed — tells us something important about the quality of the operating system running the public debate.

THE NUMBERS BEHIND THE NOISE

✦ 23 airports on federal land, leased to 21 not-for-profit airport authorities — none of them operated by the federal government in any day-to-day sense since the early 1990s.

✦ The federal government already collects up to 12% of gross airport revenues in annual rent, making Ottawa a significant financial beneficiary of the current model.

✦ Combined estimated value of these assets: approximately $100 billion — currently described as “dead capital” by Globe and Mail analysts.

✦ A 2022 study of 2,444 airports across 217 countries found passenger traffic rises 84% and per-flight efficiency improves 20% under private equity ownership.

✦ Canada’s pension funds — including the CPP Investment Board — have been lobbying Ottawa for years for access to domestic infrastructure assets their international counterparts already hold.

The government, for its part, is already extracting rent — up to twelve cents on every dollar of gross revenue these airports generate. It is not operating these facilities at a loss out of patriotic duty. It is functioning as a landlord who collects a significant cheque and then lets the tenant manage the property.

This is the foundational context that virtually no outraged commentator has bothered to establish before staking their position.

“The debate is not really about whether to privatize Canadian airports. It is about whether to change the precise legal character of a privatization that already happened three decades ago.”

— The Architect

What Is Actually Being Proposed

What the Carney government floated in the November 2025 budget, and reiterated in the April 28 spring economic update, is not a sudden sell-off. Transport Minister Steven MacKinnon used careful, measured language: the government is in the early stages of exploring alternative models of ownership. Consultations are underway with airport authorities, airlines, and municipal governments.

The options on the table range from modest to structural: extending existing lease terms, enabling commercial development on airport lands — hotels, terminals, retail — revising the rent formulas, or, at the far end of the spectrum, actual privatization in the British or Australian model. These are not the same thing. They represent a spectrum of intervention, and the government has committed to none of them.

The animating logic, stated plainly, is capital recycling. The Carney government wants to seed its new Canada Strong Fund — a $25 billion sovereign wealth fund aimed at nation-building infrastructure. Monetizing airport assets is one mechanism being explored for generating that capital without additional borrowing.

It is worth noting who else is paying close attention: Canada’s pension funds. The Canada Pension Plan Investment Board has been explicit that hub airports in G7 nations sit in the “sweet spot” for institutional investment. These are not foreign vultures. These are the funds managing Canadian retirement savings — funds that have been quietly lobbying Ottawa for years to be given access to domestic infrastructure assets that their international counterparts already invest in freely.

The optics of that last point deserve a moment’s attention. If Canadian pension capital is financing airport infrastructure in Heathrow, Sydney, and Charles de Gaulle — but is structurally excluded from doing the same at Pearson and Vancouver — that is not a sovereignty position. That is a policy incoherence. The capital is already doing exactly what critics fear; it is simply doing it abroad.

The Legitimate Concerns

None of this means the proposal is without risk. The international evidence cuts both ways, and intellectual honesty requires that both sides be named clearly.

On efficiency, the data is genuinely encouraging: private ownership correlates strongly with expansion and improved throughput. Airports get bigger. More gates. More terminals. The machinery of travel works better, moves faster, and handles volume more effectively. There is no serious dispute about this in the academic literature.

On cost, the news is less comfortable. Privatized airports tend to raise the fees charged to airlines — and airlines pass those costs directly to passengers. The deregulatory logic of private ownership also tends to erode government-imposed caps on those fees over time. The British experience, which Carney himself has pointed to approvingly, is not an unambiguous success story for the travelling public. Heathrow is world-class. It is also one of the most expensive airports on earth to fly through. Those two facts are not unrelated.

There is also a deeper structural risk that the efficiency data cannot capture: the problem of what economists call “natural monopoly.” An airport is not a coffee shop. A traveller in Toronto cannot choose a competing airport the way they choose a competing coffee chain. The competitive discipline that makes private markets function well is absent by definition. Which means that the regulatory framework surrounding any privatized airport becomes not a supplement to market forces, but the only meaningful constraint on extraction. And regulatory frameworks, in Canada’s experience, have a tendency to degrade over time as the regulated entity outresources the regulator.

There is finally the question of what happens to the proceeds. Privatization as a mechanism is only defensible if the capital released is deployed with discipline and transparency into assets of comparable or greater public value. The Globe and Mail’s editorial case — sell Pearson to fund Toronto transit; sell Vancouver International to fund SkyTrain expansion — represents the kind of explicit, auditable accountability that any such transaction should require. Vague deposits into a sovereign wealth fund governed by opaque timelines and ministerial discretion are a different matter entirely. The history of sovereign wealth funds in democratic jurisdictions is not uniformly inspiring.

“The sovereignty argument, invoked loudly, is the weakest one available. These airports stopped being ‘government-run’ before most of the people arguing the point were paying taxes.”

— The Architect

The Requisite Organization Problem

Elliot Jaques spent fifty years studying institutions and arrived at a conclusion that should be central to this debate but is nowhere in it: the capacity of an organization to govern a function well is determined by whether the cognitive complexity of its leadership matches the complexity of what it is governing.

Applied here: what level of institutional capacity does the oversight of a privatized national airport system actually require? It requires the ability to think in decades, not electoral cycles. It requires the capacity to model second and third-order effects of regulatory change across a system of interdependent hubs. It requires the kind of strategic time horizon that Jaques called Stratum VI and VII thinking — the rarest and most demanding form of organizational cognition.

Does Transport Canada currently operate at that level? Does the regulatory apparatus that would govern a privatized Pearson have the cognitive and institutional horsepower to match the legal and financial sophistication of the entities it would be regulating? These are not rhetorical questions. They are the prior questions — the ones that must be answered before the policy question can be answered responsibly.

A privatization conducted without a requisite regulatory architecture is not a policy. It is an extraction waiting to happen. And the Canadian public, operating at the level of impressions and slogans, has no framework for asking this question. It can only feel the answer after the fact, when the fees have risen and the regulator has been captured and the surplus has long since left the country.

What the Noise Cannot See

The PIAAC literacy data tells us that roughly 15% of adults in developed nations read and reason at the level where this kind of structural complexity can be properly processed. The remaining 85% — and this is not a moral judgment but a cognitive and empirical one — are operating on impressions, slogans, and tribal reflexes. “Don’t sell our airports” is a reflex. It is not an argument. It presupposes a model of ownership that no longer exists and has not existed for thirty years.

The reflex is understandable. Canadians have a legitimate and deep-seated instinct about public infrastructure. They have watched privatization in other sectors produce extraction rather than service. Hydro. Rail. Healthcare adjacents. The suspicion is not irrational — it is simply being applied here without the foundational knowledge required to apply it accurately. A calibrated instrument being used as a blunt one.

What is required, and almost entirely absent from the public conversation, is structural literacy: the ability to distinguish between what a thing is called and what it actually does. Between the word “privatization” and the specific legal and financial architecture that word is being used to describe. Between the emotion a policy triggers and the evidence the policy warrants.

Canada’s airports are already operated as commercial enterprises. The question before the Carney government is whether the legal and financial architecture governing that commercial operation should change — and if so, under what terms, with what regulatory protections, with what explicit and auditable commitment about where the proceeds go, and with what institutional capacity standing behind the oversight.

Those are serious questions. They deserve a serious public conversation. The sound and fury currently being generated suggests we are some distance from that conversation yet. But the conversation is possible. The facts are available. The frameworks exist. What is required is the willingness to put them to use.

That is what The Vertical Dispatch is here for.

✦ ✦ ✦

The Vertical Dispatch will continue to track this file as the consultation process unfolds. The first test of the Carney government’s seriousness will not be whether it privatizes — it will be whether it publishes, in plain language, a full accounting of what these assets are worth, who would buy them, on what terms, and precisely where every dollar of proceeds would go. Accountability is not a constraint on bold policy. It is the condition that makes bold policy legitimate.

Watch the terms. Not the headlines.

#CanadaAirports · #AirportPrivatization · #CarneyGovernment · #Pearson · #CanadaStrongFund · #PublicInfrastructure · #RequisiteOrganization · #ElliottJaques · #PIAAC · #StructuralLiteracy · #CapitalRecycling · #CPPIBoard · #SovereignWealthFund · #TransportCanada · #CanadianPolicy · #NaturalMonopoly · #RegulatoryCapture · #TheVerticalDispatch · #TheArchitect · #AIG · #Substack · #CanadianPolitics · #PublicDebate · #CivicLiteracy · #LongformWriting · #PolicyAnalysis · #DeadCapital · #Project2046

The Vertical Dispatch · Substack · All Rights Reserved

Yes , thank you so much for this. Too many people are so ready to label PMMC as a sellout. I wish I could restack this a hundred more times

Interesting