The Canada Strong Fund

Nation-Building or Nostalgia in a New Wrapper?

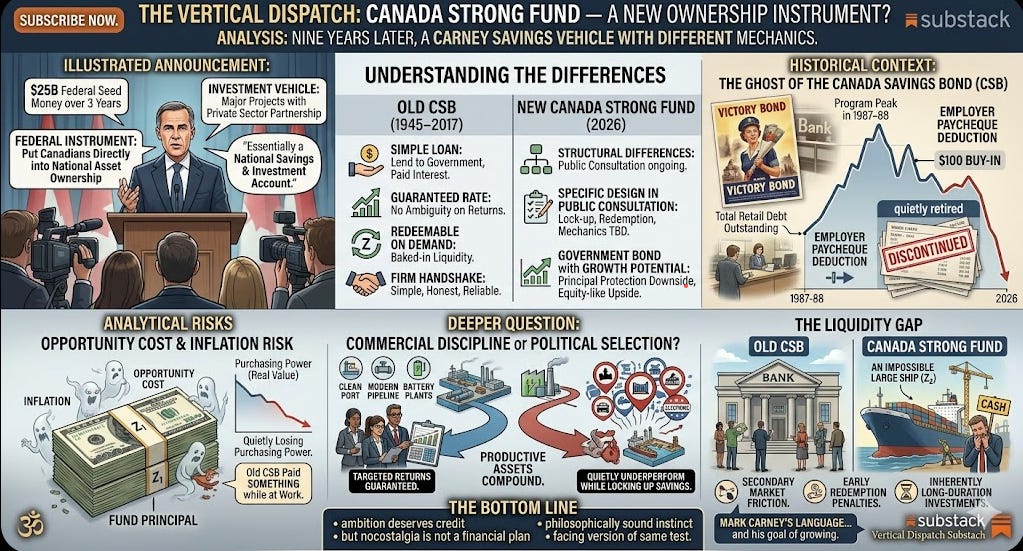

Yesterday, Prime Minister Mark Carney stood in front of cameras and announced something Canada hasn’t seen in a very long time: a federal instrument designed to put ordinary Canadians directly into the ownership of national assets.

He called it the Canada Strong Fund. It will serve as an investment vehicle to finance major projects of national interest, working in partnership with the private sector. The government will seed it with $25 billion over three years, and it will invest in strategic Canadian projects and companies alongside other investors — with a clear objective of achieving commercial returns to build the wealth of Canada.

But to understand what this actually is — and what it isn’t — you need to go back further than the press release. You need to go back to 1945.

The Ghost of the Canada Savings Bond

For more than 70 years, Canada Savings Bonds were a safe investment vehicle that provided Canadians with a guaranteed rate of return — and the government with funds for capital projects. They were first introduced after the Second World War, born from the same Victory Bond tradition that helped finance two world wars. At their peak in 1987–88, the program represented nearly $55 billion in total retail debt outstanding.

Every working Canadian of a certain generation knew what a Canada Savings Bond was. You could buy one for $100. Your employer could deduct contributions straight from your paycheque. The government guaranteed you’d get your money back, plus interest. It wasn’t glamorous. It wasn’t a stock tip. It was the financial equivalent of a firm handshake: simple, honest, and reliable.

Then the rates started falling. In 1981, CSBs offered a peak interest rate of 19.5%. By 2020, that had collapsed to 0.5%. Canadians stopped buying them. In March 2017, the federal budget officially discontinued the program. All outstanding bonds reached maturity and stopped earning interest in December 2021.

A seventy-six year tradition — quietly retired.

No replacement was offered. The government simply walked away from that relationship with the ordinary saver.

Enter the Canada Strong Fund — Nine Years Later

Carney is trying to rebuild something in that vacant space. And to his credit, he frames it in exactly those terms. He described the fund as “essentially a national savings and investment account,” saying it is designed to “grow wealth for future generations.”

But the Canada Strong Fund and the old Canada Savings Bond are not the same instrument. Understanding the differences is the whole ballgame.

The old CSB was simple: you lent the government money, it paid you interest, you could cash out at almost any time. Canada Savings Bonds were redeemable on demand — that liquidity was baked in from the beginning. The interest rate was guaranteed. There was no ambiguity about what you were getting.

The Canada Strong Fund is structurally different. The government intends to offer Canadians the opportunity to participate directly in the Fund through a new retail investment product — but the specific design is still in public consultation. We do not yet know the lock-up period, the redemption rules, or the mechanics by which any upside gets distributed to retail participants. What we do know is that Carney has described it as something like buying a government bond with growth potential: principal protection on the downside, equity-like participation on the upside.

That sounds attractive in a headline. But it contains a hidden cost that the announcement slides do not emphasize: opportunity cost and inflation risk.

If your $1,000 sits in the Fund for seven years earning no guaranteed interest while inflation runs at 2–3% annually, you have quietly lost purchasing power even if you get your nominal $1,000 back. The old Canada Savings Bond, even in its weakened final years, at least paid you something while your money was at work. The new instrument, as currently described, may pay you nothing until the underlying projects generate returns — and there is no guarantee of when or whether that happens.

The Deeper Question: Commercial Discipline or Political Selection?

The CSB comparison also illuminates a structural risk that the Fund’s architects need to answer directly.

The old savings bond program sent money into the government’s general revenues. It wasn’t pretty, but it was transparent: you lent to Ottawa, Ottawa spent it, you got interest. The Canada Strong Fund proposes something more ambitious — directing retail capital into specific productive assets: strategic Canadian projects and companies.

That is genuinely superior as a concept. Productive assets, properly chosen, compound. Ports and pipelines and battery plants generate real economic returns. A savings bond lent to pay civil service salaries does not.

The risk is project selection. For private equity investors to choose Canada, the new sovereign wealth fund will need to guarantee targeted returns. If the Fund’s investments are chosen by commercial discipline — genuine risk-adjusted return analysis — it could work. If they are chosen by political geography, by which ridings need an infrastructure announcement before the next election, it will quietly underperform while locking up ordinary Canadians’ savings.

The Fund will operate at arm’s length from government, guided by a CEO and a qualified independent board. That is the right governance architecture on paper. Whether it holds under political pressure is the question that no announcement can answer in advance.

The Liquidity Gap

There is one more dimension where the Canada Strong Fund cannot match its predecessor, and where the government needs to be completely honest with Canadians before they invest a dollar.

The old Canada Savings Bond was redeemable on demand. You needed the money, you went to the bank, you got the money. That simplicity was not incidental — it was the core of the product’s trustworthiness. Canadians parked emergency savings in CSBs precisely because they knew the money was accessible.

The Canada Strong Fund, by its nature, cannot offer that. The underlying investments — large infrastructure projects and domestic companies — are inherently long-duration. You cannot liquidate a mine or a port on a Tuesday afternoon because a retail investor needs cash. Some form of secondary market may develop over time, but it will carry friction, bid-ask spreads, and potentially early-redemption penalties.

For a conservative saver who understands and accepts that trade-off, the Fund may still be attractive. For someone who confuses it with the old savings bond because the government is using similar patriotic language, it is a potential trap.

The Bottom Line

The Canada Strong Fund is the most serious attempt since 1945 to reconnect ordinary Canadians with the ownership of national productive assets. That ambition deserves credit. The instinct behind it — that Canadians should be stakeholders in the infrastructure that generates the country’s wealth, not just taxpayers who finance it — is philosophically sound.

But nostalgia is not a financial plan. The Canada Savings Bond was not discontinued because the government lost interest in retail savers. It was discontinued because the rates became uncompetitive and Canadians stopped buying. Declining sales and escalating administrative costs made it less financially practical.

The Canada Strong Fund will face a version of the same test. If the retail product offers genuine returns, reasonable liquidity, and transparent governance, Canadians will participate. If it offers principal protection wrapped in a lock-up period while inflation quietly erodes real value, it will be the 0.5% savings bond in a new coat.

Mark Carney knows the difference. He has described the Fund’s goal as growing “through asset recycling and reinvestment, creating even greater opportunities for future generations.” That language comes from someone who understands long-duration capital. The question is whether the political incentives of the institution he now leads will allow him to build the disciplined, genuinely commercial vehicle he is describing.

The Spring Economic Update lands today. We will know more by evening.

Glen Roberts publishes The Vertical Dispatch on Substack. He is the author of Sacred Metaphysics and Consciousness: History of the Absolute and Eternal, and the developer of the Universal Dynamics framework and AIG — Artificially Intelligent Governance.

#CanadaStrongFund #MarkCarney #Carney #CanadianEconomy #CdnEcon #CanadaFinance #CdnPol #CdnPolitics #SovereignWealthFund #RetailInvestment #AssetOwnership #NationalAssets #PublicPrivatePartnership #Infrastructure #CanadaSavingsBonds #CSB #VictoryBonds #EconomicHistory #InvestmentAnalysis #OpportunityCost #InflationRisk #LiquidityGap #CommercialDiscipline #PoliticalSelection #LongDurationCapital #EconomicUpdate #Substack #TheVerticalDispatch #VerticalDispatch #DeepDive #Analysis

Do we know more? Will this be RSP eligible, or does the lack of liquidity prevent that? What does this mean for Canadians wanting to divest from fossil-fuel industry and infrastructure?