The Emperor Wears No Clothes

How the Adults in the Room Are Quietly Reorganizing the World While Smiling at the Man with the Tariffs

The Sovereign Core · The Age of Consequences

Keystone Geopolitical Dispatch · May 29, 2026

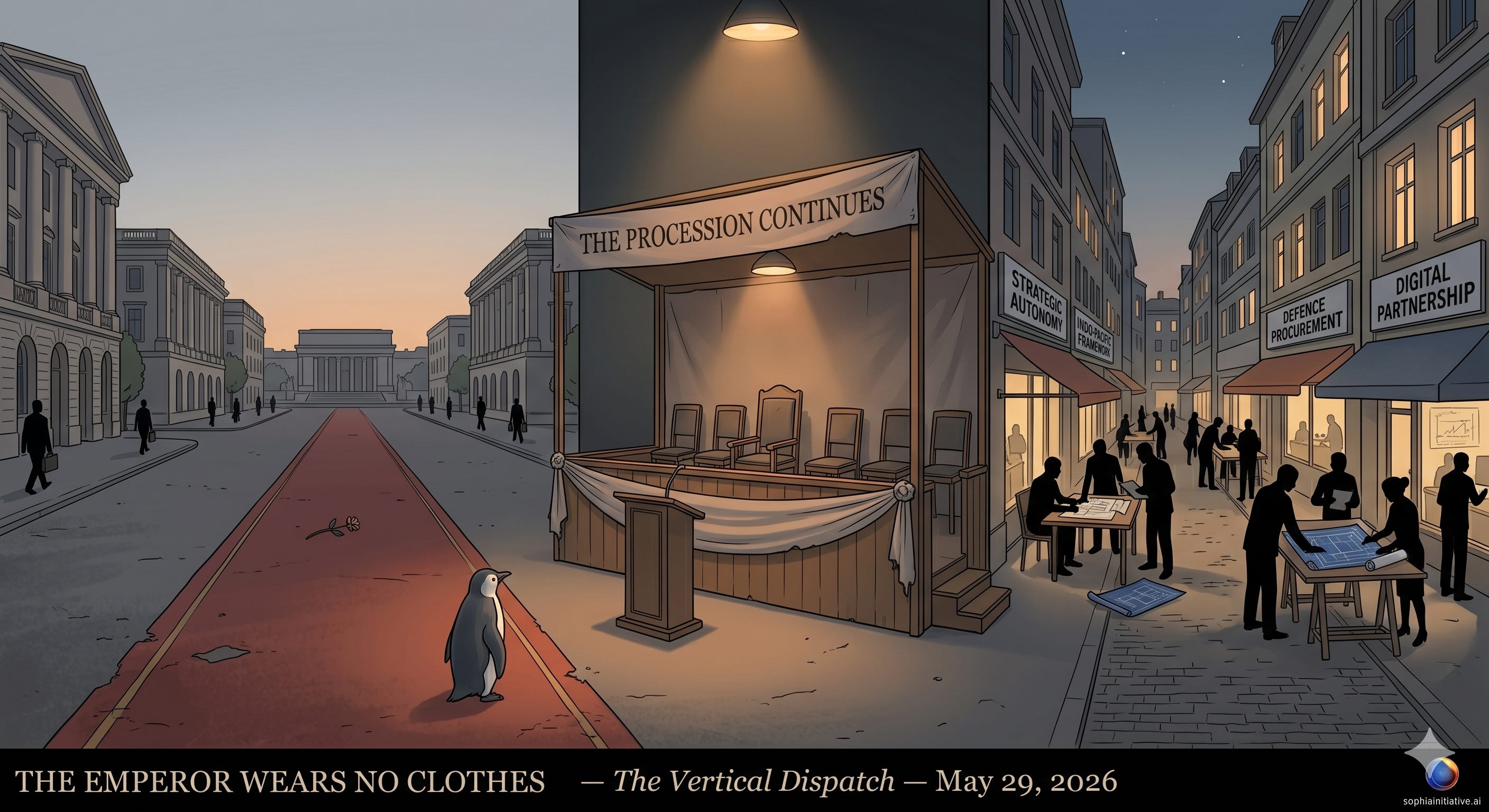

“And so it happened that the Emperor walked in the procession under the beautiful canopy,

and all the people in the streets and at the windows said: ‘How beautiful the Emperor’s new clothes are!’

And no one would confess that he saw nothing, for he would have been said to be either a fool or unfit for his office.”

— Hans Christian Andersen, 1837

On April 2, 2025, the President of the United States signed an executive order imposing tariffs on the Heard Island and McDonald Islands. The territory is a sub-Antarctic Australian external possession. Its population, in the most recent count, consists of approximately one million penguins, several thousand seals, and zero human beings. The territory has no economy. It has never traded with the United States. The tariff was set at ten percent.

The same order tariffed the British Indian Ocean Territory at ten percent. That territory has no civilian economy either; the only human presence is the military personnel stationed at Diego Garcia. The order tariffed Christmas Island at ten percent, the Cocos Keeling Islands at ten percent, the French Southern and Antarctic Lands at ten percent, and Norfolk Island, for reasons no one in the administration was subsequently able to explain, at twenty-nine percent. It also tariffed the United States Minor Outlying Islands at ten percent — which is to say, the United States imposed a tariff on itself.

Asked to explain on April 7, 2025, Commerce Secretary Howard Lutnick told reporters that the list had been generated algorithmically from the United States Trade Representative’s database without manual review, and that the inclusion of uninhabited territories was a precautionary measure to close off any possible loopholes. The London Economic ran the headline “Trump puts tariff on island only populated by penguins.” LBC ran the headline “No one is safe, not even the penguins.” The world’s serious financial press recorded the event with a single shared expression. The expression was the same expression worn by the small child in the Hans Christian Andersen story when he first saw the emperor walking past.

This dispatch is about that child. It is also about the adults — and there are many — who were standing in the street that day, who saw exactly what the child saw, and who chose, for reasons of protocol and self-interest and the practical demands of statecraft, to say nothing. The dispatch is about what those adults have been doing in the sixteen months since, while the procession has continued and the emperor has continued to walk and the official protocol has continued to require everyone to comment favourably on his magnificent garments. Because while the procession has been proceeding, the adults have been doing something else entirely. They have been quietly reorganizing the world.

I. The Procession — Seventeen Tariff Regimes in Sixteen Months

The documented record of what has happened to United States trade policy between January 20, 2025 and May 29, 2026 is, as a matter of empirical fact, the most chaotic episode of trade-policy administration in the post-war history of the international system. The dispatch will not editorialize this claim. The dispatch will lay the record.

Seventeen distinct tariff regimes have been imposed in sixteen months. Seven of them were imposed under the International Emergency Economic Powers Act, the same statute Congress passed in 1977 to authorize sanctions against hostile foreign actors. The IEEPA framework was used to declare a series of national emergencies — fentanyl flows, migration pressures, large and persistent United States goods trade deficits, the political persecution of former Brazilian president Jair Bolsonaro, and the continued purchase of Russian Federation crude oil by India — and to use those emergency declarations as the legal basis for sweeping tariff actions affecting nearly every trading partner of the United States.

On February 20, 2026, the Supreme Court of the United States, in a six-to-three decision in Learning Resources, Inc. v. Trump, ruled that the International Emergency Economic Powers Act does not authorize the President to impose tariffs. The Court held that the statute’s authority to “regulate ... importation” does not include the power to levy duties, and that tariff authority remains with Congress unless Congress has explicitly delegated that authority. The opinion was joined by both conservative and liberal justices. Collection of all seven IEEPA tariff regimes was halted by Customs and Border Protection at 12:01 a.m. on February 24, 2026. As of May 27, 2026, the United States Treasury had paid over twenty billion six hundred million dollars in refunds to importers, with an estimated additional eighty-five billion dollars in certified refunds pending.

Twenty billion dollars in refunds, paid in cash, to importers who had been required to pay duties that the highest court in the United States ruled the President had no authority to impose. The number, by itself, is the empirical statement of what the past sixteen months have cost. It is also the statement of what the international system has been quietly assessing as it has gone about its work.

Seven additional tariff regimes have been imposed under Section 232 of the Trade Expansion Act of 1962, the national security provision. The Section 232 tariffs cover steel and aluminum at fifty percent of full value, copper at fifty percent, lumber and wood products at rates ranging from ten percent to fifty percent, advanced semiconductors at twenty-five percent, and patented pharmaceutical products at one hundred percent. Two Section 301 regimes cover Chinese strategic sectors — shipbuilding, mature-node semiconductors, medical supplies — at rates up to one hundred percent. One regime, under Section 122 of the Trade Act of 1974, imposes a temporary ten percent global tariff on all imports, partially enjoined by the Court of International Trade on May 7, 2026, in Oregon v. United States. The Section 122 tariff expires on July 24, 2026, unless Congress extends it. Congress, at the time of this writing, has not signaled that it will.

The cumulative record is, by any honest measurement, an extraordinary spectacle. Tariffs imposed, tariffs paused, tariffs doubled, tariffs reduced, tariffs reciprocated, tariffs litigated, tariffs struck down, tariffs replaced, tariffs threatened, tariffs unannounced, tariffs imposed on uninhabited islands, tariffs imposed by the United States on itself. Twenty billion in refunds paid. Eighty-five billion pending. Sixteen months. The procession has been spectacular. The procession has also been, as the small child in the story observed and as the global financial press has now repeatedly recorded, naked.

II. The Adults in the Street

This is where the dispatch parts company with the conventional commentary on the trade war, because the conventional commentary, which has fixated on the spectacle of the procession, has missed the more important story. The more important story is what the people standing in the street have been doing while the procession passed.

There were, throughout the sixteen-month period, a small number of public officials and finance ministers and central bankers and heads of state who, in their own languages and at their own desks, recognized the procession for what it was. They did not say so publicly. The protocol forbade it. To say publicly that the emperor was naked would have produced an immediate retaliatory escalation, an interruption of bilateral relations, and a domestic political cost in their own countries that none of them could afford to pay. So they smiled. They negotiated. They flew to Mar-a-Lago when summoned. They issued joint statements that said the relationship was strong and the cooperation was productive and the framework was being finalized. And they walked, calmly and deliberately, out of the showroom into the parking lot, and into the other showrooms across the street, where the architecture of the next century was being quietly built between them.

This is not interpretation. This is the documented record. Between January 2025 and May 2026, while the United States was imposing and reimposing and litigating its seventeen tariff regimes, the same period saw the conclusion of the European Union’s Turnberry framework agreement with the United States in July 2025 — at a fifteen percent ceiling, half the threatened rate, with explicit provisions for non-retaliation and for the eventual lifting of Section 232 metals tariffs. The same period saw Japan and South Korea each conclude framework agreements at fifteen percent ceilings — with Japan committing five hundred and fifty billion dollars and South Korea three hundred and fifty billion dollars in investment, on terms the two governments were able to write into the agreements because the United States needed the deals more than the two governments needed them. The same period saw Vietnam, Malaysia, Cambodia, and Thailand each negotiate frameworks that reduced their threatened tariff rates by half or more. The same period saw the November 4, 2025 China truce, in which Beijing agreed to reduce fentanyl-precursor flows and the United States agreed to reduce its tariffs — a political truce, not a treaty, but a truce that has held.

And the same period, the same exact sixteen months, saw something else, which the conventional commentary has consistently underweighted. It saw the most significant burst of non-American bilateral and multilateral architecture-building among the world’s serious middle powers and major economies since the founding of the European Union itself. While the procession proceeded down the main street, the adults in the side streets were doing the actual work of statecraft.

III. Carney, the Bank of England, and the Customer in the Showroom

The Vertical Dispatch has, in recent dispatches, described Canada’s posture in the bilateral trade relationship with the United States through the metaphor of the customer in a used-car showroom, reading the contract calmly while the salesman gesticulates at the rusted 2020 model on the lot. The metaphor stands. The customer is Prime Minister Mark Carney. The customer’s posture is that of a man who has held, across two decades of public service at the Bank of Canada and the Bank of England and the United Nations and the Financial Stability Board, the disciplined cognitive operation that Elliott Jaques called a Stratum Eight time horizon. He sees the long board. He sees the short board. He plays them at the same time.

Carney, in private and in public, has been doing both games simultaneously since taking office in March 2026. With Washington, he has played the protocol — the smile, the joint statement, the careful press conference, the refusal to chase a small deal. With Tokyo, Berlin, Paris, London, Stockholm, Seoul, Canberra, and the European Commission, he has been playing the chess game that the protocol with Washington permits him to play in parallel. The May 27, 2026 announcement of the Saab GlobalEye procurement — six aircraft, five billion Canadian dollars, chosen over the Boeing E-7A and the L3Harris Aeris X, with forty additional aircraft to be built in Canada by Bombardier and three thousand jobs created — is, viewed in isolation, a defence procurement decision. Viewed in the context of this dispatch, it is the most visible single move in a much larger consolidation.

Stephanie Carvin and Philippe Lagassé, two of Canada’s most serious public-record defence analysts, both said openly in CBC and Globe and Mail interviews on the day of the announcement that the Saab choice was the first major step in the diversification of Canadian defence procurement away from the American defence-industrial base. Lagassé’s exact words: “It is the first step in demonstrating diversification beyond American defence industry.” That sentence, said publicly, by a Canadian academic specialist, on the public record, is what every Canadian foreign minister and every Canadian deputy minister has been thinking for fourteen months. It is also what every European and Indo-Pacific counterpart of those Canadian officials has been thinking. The Saab announcement is the moment when one of the adults in the street took out a tape measure and began openly measuring the emperor’s procession against the actual width of the street. The other adults watched. The other adults are now reaching for their own tape measures.

IV. The Architects, the Hedgers, the Captives, the Witnesses

The dispatch will now offer a working taxonomy of how the world’s middle and major powers have positioned themselves during the sixteen-month period. The taxonomy is offered as a working frame, not as a final classification. The categories are: the Architects, the Hedgers, the Captives, and the Witnesses. Each category names a posture rather than a permanent identity. Some actors move between categories. The categories themselves will continue to develop as the architecture continues to consolidate.

The Architects

The Architects are the powers that are openly, on the documented record, building the post-American economic architecture. They are not announcing the building. They are doing the building, in framework agreements and procurement decisions and investment commitments and bilateral treaties that have, individually, the form of routine statecraft and that, collectively, form the bones of the order that is being assembled.

The European Union is an Architect. The Turnberry framework with Washington sets a fifteen percent ceiling on most EU exports — a defensive perimeter, not an embrace. Inside that perimeter, the EU has, in the same sixteen-month period, completed the long-delayed Capital Markets Union infrastructure, ratified the EU-Mercosur trade agreement after twenty-five years of negotiation, signed the digital partnership with Japan, and committed to the strategic autonomy doctrine the European Commission has been quietly articulating since the second Trump term began. The European Parliament’s approval of the Turnberry framework on March 26, 2026, was less an embrace of the United States than a procedural step to keep the trade relationship from imploding while the rest of the architecture is built. The EU has been an Architect since 2017. It is now an Architect with a published doctrine and a procurement pipeline.

Japan is an Architect. The five hundred and fifty billion dollar investment commitment in the August 2025 framework looks, on the surface, like a concession. Read carefully, the investment is a hedge against the prospect that the United States may, in three years or seven years, no longer be a reliable partner. Japan is buying a stake in the United States economy at a moment when Japan can write the terms of the stake. It is the same instinct that produced the Plaza Accord generation of Japanese direct investment in American manufacturing in the 1980s, deployed at the next civilizational scale. Japan is also, simultaneously, deepening its Indo-Pacific quad-plus architecture with India, Australia, South Korea, and the Philippines, and is, in May 2026, completing the legal preparations for a Japan-EU defence-industrial cooperation framework that was unthinkable five years ago. Japan is doing checkers with Washington and chess with everyone else. Japan is an Architect.

South Korea is an Architect. The three hundred and fifty billion dollar investment commitment is the same hedge as Japan’s, scaled to Korean industrial capacity. Beneath it, Korea has been quietly accelerating its defence-export relationships with Poland, Romania, the Philippines, and Saudi Arabia, while deepening its supply-chain integration with the European Union and Japan. South Korea is, in May 2026, the world’s fastest-growing arms exporter. That is not coincidence. That is the consequence of an Architect’s deliberate work.

Canada is an Architect, and the dispatch has named the evidence above. The Saab procurement. The five-year, trillion-dollar capital plan. The Carney cabinet’s quiet diplomacy with the EU, Japan, Korea, and Australia. The refusal to chase the small CUSMA deal. The Architect status was earned by the cognitive stratum of the leadership and confirmed by the leadership’s first ninety days in office. Canada is now, in the documented record, an Architect at a scale that no Canadian prime minister has occupied since Lester Pearson in the 1960s.

Australia is an Architect. The AUKUS submarine program — controversial, expensive, delayed — has nonetheless committed Australia to a thirty-year industrial cooperation with the United Kingdom and to a parallel relationship with the United States that Australia can adjust as conditions require. The May 2026 announcement of the Australia-Japan-Philippines-India quadrilateral fishery and maritime-security framework, signed in Manila, is the kind of routine middle-power statecraft that, in the aggregate, becomes architecture. Australia is also, quietly, the largest single non-Chinese supplier of critical minerals to the post-American supply chain that is being assembled. The strategic significance of that fact is becoming visible at a pace the conventional commentary has not yet metabolized.

The Hedgers

The Hedgers are powers playing both boards openly. They are not yet Architects in the full sense — their commitments to the post-American architecture are conditional, reversible, and instrumental — but they are also no longer Captives. They are using the present moment to maximize their optionality, on the principle that a middle power that hedges well in a structurally uncertain decade will be a more powerful middle power at the end of the decade than one that committed early to either side.

India is the largest Hedger. The February 2026 termination of the Russian-oil penalty tariff was the public sign of a quiet commitment: India will stop directly buying Russian crude in exchange for a framework agreement on the bilateral trade relationship with the United States. The framework has not been signed as of May 29, 2026. Negotiations continue. Meanwhile, India has continued to expand its defence-procurement relationships with France, with Israel, with Russia in legacy contracts, and with itself through accelerated domestic-production targets. India is also, in the same sixteen-month period, the single largest beneficiary of the realignment of supply chains away from China — Apple’s manufacturing pivot, Samsung’s expansion, Foxconn’s investments. India is hedging at extraordinary scale. India will, when the dust settles, be one of the great winners of the present moment. India is a Hedger now and will be an Architect within five years.

Vietnam, Malaysia, Cambodia, Thailand, and Indonesia are Hedgers. The ASEAN bloc has, in the sixteen-month period, accelerated its own internal integration while individually negotiating bilateral frameworks with Washington that reduce their immediate tariff exposure. The Comprehensive and Progressive Trans-Pacific Partnership — a treaty the United States abandoned in 2017 — has continued to deepen, with the United Kingdom acceding in 2024 and active discussions for South Korean and Indonesian membership in 2026. The ASEAN-EU and ASEAN-UK framework agreements are quietly being upgraded. The Hedgers of Southeast Asia are using American distraction to consolidate their own regional architecture at speed.

Mexico is a Hedger in a complicated position. Inside USMCA, Mexico is structurally bound to the American economic architecture. President Claudia Sheinbaum has, in eight months in office, played a masterclass in protocol — the smile with Washington, the cooperation on migration, the joint statement on fentanyl precursors — while simultaneously expanding the Mexican supply-chain integration with Brazil, with the EU, with Japan, and with the People’s Republic of China at a tempo that has produced more new bilateral commercial agreements in eight months than the previous administration produced in six years. Mexico is doing both games at high speed, and the result will be a Mexico in 2030 that is dramatically less dependent on the United States than the Mexico of 2024 was — without ever having said so out loud.

Switzerland, Norway, Liechtenstein, and the smaller European non-EU states are Hedgers. The thirty-one percent rate Switzerland received on April 2, 2025, was higher than the rate imposed on the EU itself, which signals that Switzerland’s position outside the EU procurement architecture made it more vulnerable. Switzerland has, since then, accelerated its integration with EU regulatory and procurement frameworks while maintaining its formal independence — a Hedger’s classic posture.

The Captives

The Captives are powers whose domestic political alignment with the American administration has prevented them from positioning for the post-American architecture. They have chosen, for ideological or transactional reasons, to remain inside the procession. The dispatch will name the category without lingering on it, because the future of the Captive states is the future the next dispatch will need to address.

Argentina under President Javier Milei is a Captive. The Milei government’s deliberate ideological alignment with the Trump administration produced, in the first year, public expressions of solidarity and a closer bilateral relationship with Washington than any previous Argentine government. It has not produced any of the framework benefits that the Hedgers and Architects have negotiated. Argentina pays the Section 122 ten percent tariff on the same terms as Brazil. Argentina has received no investment commitment, no defence-procurement opportunity, no preferential framework. The relationship is rhetorical. The relationship is also, in the assessment of the present dispatch, a category error that future Argentine governments will need to reverse at significant cost.

Hungary under Prime Minister Viktor Orbán is a Captive. The Orbán government has positioned itself as the European voice closest to the Trump administration and has, in consequence, been excluded from the post-American architecture being built around it by the rest of the European Union. Hungarian access to the EU’s strategic autonomy procurement pipeline is constrained. Hungarian participation in the EU-Japan defence-industrial framework is constrained. Hungary, like Argentina, has chosen the procession. The procession’s costs are now becoming visible to the Hungarian electorate.

The Captive category is small and is, on the present trajectory, becoming smaller. The political-cost calculus of remaining inside the procession is being recalculated in every Captive capital. The dispatch leaves the names of the additional possible Captive transitions to a future piece.

The Witnesses

The Witnesses are powers that have, on the public record, openly named the procession for what it is. They have not joined any new architecture. They have not signed framework agreements with Washington. They have, instead, used their international platforms to bear witness to what the documented record shows.

Brazil under President Luiz Inácio Lula da Silva is a Witness. The fifty percent IEEPA tariff imposed by Washington on July 9, 2025, in retaliation for what the United States described as the persecution of former president Jair Bolsonaro, was struck down on February 20, 2026, alongside all other IEEPA tariffs. Brazil has, in the interim, refused to sign a bilateral framework agreement. Brazil has filed a WTO challenge. Brazil has used its BRICS-plus chairmanship to articulate, in unusually plain language, the case for an international system that does not accept arbitrary tariff actions as a substitute for treaty-based commerce. Brazil’s posture is the witness’s posture: the record will speak, the record will be heard, and the future will assess. Brazil is also, the dispatch notes carefully, doing significant quiet bilateral work with Canada, Mexico, the EU, China, and India — Witness in public, Hedger in practice.

South Africa is a Witness. The thirty percent reciprocal IEEPA tariff imposed on April 2, 2025, was higher than the rate imposed on most peer economies. The South African government has used the experience to deepen its International Court of Justice work, its BRICS-plus diplomacy, and its African Union leadership on the question of a continental industrial policy that does not depend on American goodwill. South Africa is a Witness with significant moral capital. The moral capital is being deployed.

Ireland is a Witness in a quieter register. The Irish government has, on Gaza and on Iran, used its EU membership and its small-power moral platform to articulate positions that the larger European powers have been politically unable to articulate. Ireland is not building post-American architecture in the procurement sense. Ireland is doing something else equally important: it is keeping alive, in the EU’s working vocabulary, the principles the Architects will need when the architecture is complete.

V. The Saab Signal and What Comes Next

The May 27, 2026 Saab GlobalEye announcement is, viewed in the framework above, the most important diagnostic event of the past sixteen months. The Saab choice is not, in itself, civilizational. The Saab choice is the visible sign of a civilizational decision. Canada — the Architect closest to the American procurement system, the Architect most economically integrated with the United States, the Architect with the most to lose by visibly choosing diversification — chose the Swedish aircraft over the American aircraft, on the public record, in the announcement at CANSEC, with the Prime Minister and the Defence Minister and the head of Saab on stage together. The signal, sent to Berlin and Tokyo and Seoul and Paris and Stockholm, was clear. The signal, received in those capitals, was equally clear.

The other Architects will now move at increased speed. The European Union will accelerate the strategic autonomy procurement pipeline. Japan will accelerate the defence-industrial framework with the EU. South Korea will accelerate the arms-export relationships with Eastern Europe. Australia will accelerate the AUKUS-adjacent procurement decisions that have been waiting for a peer to move first. The Hedgers will watch the Architects and adjust. The Captives will watch the Hedgers and reconsider. The Witnesses will continue to bear witness and continue to do their quiet bilateral work.

The procession in Washington will continue. The emperor will continue to walk. The protocol will continue to require everyone to comment favourably on the magnificent garments. But the streets will get a little emptier each month. The adults will gradually finish their work in the side streets and walk into the new buildings together. And one morning — the dispatch will not predict the morning — the procession will arrive at the end of the parade route and discover that there is no one left in the reviewing stand. The reviewing stand will have been moved. The architecture will have been completed without the emperor’s attendance or consent. The emperor will continue to walk. There will not be anyone left who needs the emperor to walk anywhere in particular.

That is the trajectory the documented record suggests. The dispatch does not predict the timing. The dispatch names the direction.

VI. The Open Question

There remain, in honesty, two possible futures the present record can produce. The Vertical Dispatch will name both.

The first possible future is the one this dispatch has just described: the gradual, deliberate, multi-actor consolidation of a post-American architecture by the Architects and the Hedgers, with the Witnesses bearing public witness and the Captives slowly recalculating their positions. In this future, the international system metabolizes the present moment, learns what it needs to learn, builds what it needs to build, and emerges in the early 2030s with a more distributed, more resilient, more values-based order in which the United States remains a great power but no longer the singular hegemon. The architecture proceeds without the United States’s permission. It also proceeds without the United States’s destruction. This is the calm future. It requires patience, discipline, and the consistent application of the protocol at every desk in every capital that matters. The Architects are equipped to do this work.

The second possible future is the one in which the procession, sensing that the architecture is being built without it, attempts to interrupt the architecture by means more disruptive than tariffs. This future is the one the trilogy on the Iran war began to map. The eight victory declarations in ninety days, the threat to resume “with much higher intensity,” the May 27 cabinet meeting in which the President asked whether the war should be reopened — all of these are signals that the empire’s response to architectural displacement may be kinetic rather than commercial. The dispatch does not predict this future either. The dispatch names that it is on the documented record as a live possibility. The Architects are aware of it. The Architects’ procurement decisions — Saab, the European strategic autonomy doctrine, the Japan-EU defence-industrial framework, the Korean arms-export acceleration — are, in part, hedges against this possibility. The chess game is also a defensive operation.

Which future actually arrives will depend on choices that have not yet been made, in capitals that include Washington but are not limited to it. The Vertical Dispatch will continue to watch the documented record and to name what the record shows. The Architects will continue to build. The Hedgers will continue to hedge. The Witnesses will continue to bear witness. The Captives will, in their own time, make their own choices.

The emperor will continue to walk. Whether his procession arrives at any destination that the world recognizes will be answered by the world, in its own time, in the architecture it is even now completing without him.

God is Love. Love is Truth. Truth is Consciousness. Consciousness is Brahman.

Amen. Namaste. Om Namah Shivaya.

— The Architect

The Hungary Report by Peter Doza on Substack offers in-depth coverage of their transition. I haven’t seen comparable coverage in Canadian media.

Acknowledge your comparison of Carney to Pearson. I’ve forwarded this post to one of the Pearson family.