The Runway Without a Plane

The Carney-Smith Deal, the TMX Nobody Will Buy, and the Accountability Question Both Governments Refused to Answer

Sovereignty · Governance · Consequence

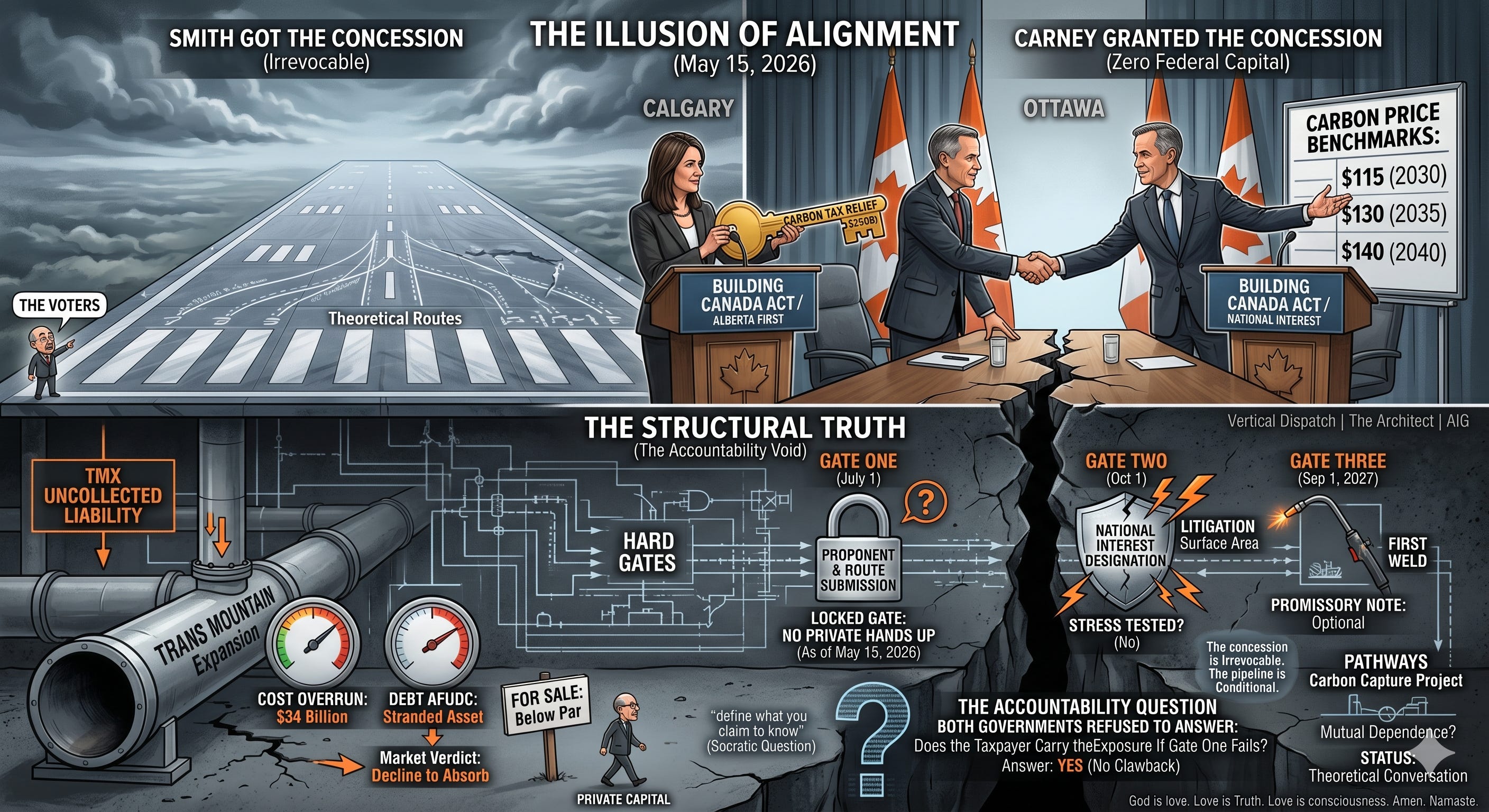

The announcement landed on May 15, 2026, with the full ceremony the political class reserves for its most useful illusions. Premier Danielle Smith and Prime Minister Mark Carney, standing together in the productive fiction of federal-provincial alignment, declared that Canada would build a new West Coast bitumen corridor — one million barrels per day, sovereign in design, decisive in intent.

The financial press called it a breakthrough. The energy sector called it encouraging. The capital markets said nothing, because capital markets do not speak; they allocate. And on May 15, 2026, they allocated nothing.

That silence is the story. And behind it sits a second silence that neither government mentioned: the Trans Mountain pipeline — the one Canada already built, the one that cost $34 billion, the one that runs today — has no buyer. No private syndicate will purchase it at par. The pipeline runs. The economics do not. Smith and Carney announced a new pipeline on the day the old one remains a stranded sovereign asset that the market has already declined to absorb. That is not a footnote. That is the context.

I. The Inventory of What Does Not Exist

Before the architecture of the deal can be understood, the inventory of its absences must be conducted with precision.

There is no private proponent. No midstream giant, no corporate consortium, no private equity syndicate has signed a construction agreement, an underwriting contract, or a binding letter of intent. The Oil Sands Alliance — the body most prominently positioned in the announcement’s narrative frame — is functioning as a policy advisor. It is not a financial underwriter. These are categorically different roles, and conflating them is the announcement’s central rhetorical sleight of hand.

There is no route. Alberta is evaluating five theoretical corridors. Without a locked route, there is no right-of-way cost, no civil engineering profile, no permitting universe, and therefore no capital cost. A pipeline without a route is not a pipeline. It is a direction.

There is no port infrastructure commitment at the receiving terminus. A one-million-barrel-per-day throughput system terminating at an undersized or non-existent marine facility is a pipe to nowhere.

The state has built a runway. The private sector has not purchased the aircraft, contracted the crew, or filed a flight plan. And the private sector already declined to purchase the last plane the state built for it.

This is the structural truth behind the headline. Not corruption, not conspiracy — simply the condition of a regulatory framework agreement being mistaken, deliberately or otherwise, for a capital formation event. Smith got what she came for before the first weld is struck. The industry retained the lower carbon price trajectory on the day of the announcement. The pipeline remains optional. The concession was not.

II. The Ghost Nobody Mentions — Trans Mountain

Every serious analyst of the Carney-Smith deal must begin with Trans Mountain because Trans Mountain is not ancient history. It is the active psychological condition of every private infrastructure capital allocator in North America who watched it unfold, and it is the living proof that the problem the new deal claims to have solved has not been solved.

The Trans Mountain Expansion entered regulatory review in 2013. It entered construction — with a fully nationalised balance sheet after Ottawa purchased the pipeline for $4.5 billion in 2018 — in 2019. It achieved completion and initial commercial operation in 2024. The final capital cost: approximately $34.9 million CAD per kilometre across a 980-kilometre corridor. Total realisation: north of $34 billion on a project originally scoped at roughly $5.4 billion.

The pipeline is operational. It is moving oil. It is generating revenue. And no private buyer will purchase it at the price it cost to build. The federal government has been attempting to sell Trans Mountain since completion. The offers that have come in are below par — sometimes significantly below. The reason is not the engineering. The reason is the debt load. The Allowance for Funds Used During Construction — AFUDC in the financing lexicon — is the mechanism by which delay becomes its own cost centre. Every year a project sits in litigation, environmental review, or jurisdictional dispute, the interest on borrowed construction funds compounds. TMX’s decade-plus regulatory gauntlet compounded AFUDC to the point where the regulated toll structure cannot service the debt at a rational return for a private buyer.

Private syndicates will not buy Trans Mountain at par. The pipeline runs. The economics do not. Canada spent $34 billion of public money building a pipeline the private sector will not buy at cost. On the day Carney and Smith announced the next pipeline, this one sat unsold on the federal balance sheet. Neither of them mentioned it. That omission is not accidental. It is the most important fact in the room.

The cost overrun is not a story of engineering failure. It is a story of temporal compounding. Under standard North American onshore construction conditions, a pipeline of TMX’s scale should cost between $5 million and $8 million per kilometre. The entire gap between that figure and the $34.9 million realised is attributable not to steel or labour, but to time — regulatory time, legal time, jurisdictional time. Every year added to the execution window is a year of AFUDC compounding. TMX added approximately eight years to its original execution window. The mathematics of compounding did the rest.

The one project, one review provision embedded in the Building Canada Act framework is the mechanism designed to foreclose that temporal trap for the new pipeline. Its effectiveness has not been tested. The litigation velocity of the modern environmental and Indigenous rights landscape has not changed because a Prime Minister and a Premier shook hands. Section 35 consultation obligations remain constitutionally binding regardless of federal policy declarations. The five unresolved routing options each carry a different Indigenous rights profile and a different litigation surface area. None of that complexity disappeared on May 15, 2026.

Private capital knows all of this. The capital community that watched TMX absorb a decade of legal attrition and emerge as a stranded sovereign asset will not sign construction agreements on the basis of a framework that has not yet been stress-tested. They will wait. They will watch Gate Two and the first legal challenge against the national interest designation. They will decide then. The announcement was not aimed at them. It was aimed at voters in Alberta.

III. The Fiscal Physics — What Ottawa Actually Did

The federal government is spending zero dollars in direct capital outlay on this project. That fact alone reframes the entire announcement. If this is not a spending commitment, what is it? It is a liability transfer mechanism — and the liability being transferred belongs to the public, not to industry.

To understand the magnitude of what has actually changed, consider the alternative trajectory. Alberta froze its industrial carbon emission price at $95 per tonne last year. Under the previously legislated national schedule, that would have risen to $170 per tonne by 2030. Under the Carney-Smith framework, the new benchmarks are $115 per tonne in 2030, $130 by 2035, and $140 by 2040. The original MOU had committed to $130 by 2030. That commitment has been extended by ten years.

The province estimates the new pricing trajectory will save the industry approximately $250 billion by 2050. That is Alberta’s number — the estimate produced by the beneficiary of the concession. It is not an audited figure. It is not an independent economic analysis. It is the industry’s projection of costs avoided, presented as the headline measure of what this deal is worth. Every outlet ran it without attribution to its source.

What the Independent Data Actually Shows

The Canadian Climate Institute — Canada’s independent climate policy research body — has spent two years documenting what industrial carbon pricing actually costs the oil sands in practice. Their findings are precise and they are devastating to the $250 billion narrative.

Oil sands producers currently pay an average of 9 cents per barrel under the existing system. Nine cents. On a barrel of Western Canadian Select trading at approximately $80. That is 0.1 percent of the commodity price. The headline carbon price is $95 per tonne. The actual per-barrel cash cost to producers, after the system’s design features — intensity benchmarks, credit markets, royalty and tax deductions — is nine cents.

If the policy had been strengthened to ensure credits traded at $130 per tonne by 2030, as the original schedule required, the per-barrel cost would have risen to approximately 50 cents. The cost of a Timbit, after inflation. The Canadian Climate Institute reviewed 17 years of provincial trade data covering 10 provinces and 19 industrial sectors and found no statistically significant evidence of export contraction linked to carbon pricing. The average estimated effect was indistinguishable from zero. The competitiveness argument that drove this deal is not supported by the empirical record of the policy it just relaxed.

The $250 billion figure is the industry’s estimate of costs avoided. The independent measure of actual cash cost to producers is 9 cents per barrel today and 50 cents by 2030. Both numbers are true. They describe the same policy from different vantage points. The gap between them is the gap between the political argument and the economic reality. Smith presented the $250 billion figure. Carney accepted it. No one at the press conference corrected it. No questions were taken.

What the federal government actually gave up is the leverage to require Alberta’s industrial carbon price to reach $170 per tonne by 2030 — costs that would have recycled through Alberta’s own TIER climate fund into emissions reduction projects, not into federal accounts. Ottawa was never collecting $250 billion. It cancelled a future obligation imposed on an industry that is now expected to voluntarily deploy a portion of the retained capital into a pipeline Ottawa cannot build without them.

IV. The Capital Variance Matrix — Best Case, Worst Case, Real Case

Infrastructure financing is not a fixed-cost problem. It is a temporal risk problem. The capital cost of the new pipeline is not determined by the price of steel or the wage rate of welders in northern British Columbia. It is determined by how long it takes to build. Model the extremes against a 1,000-kilometre corridor at one million barrels per day of design capacity.

The Sovereign Express Scenario

Federal regulatory shield holds. Route locks on schedule. Proponent consortium emerges in Q3 2026. First weld September 2027. Commercial operation September 2030. Capital cost in the range of $9 billion. AFUDC remains a minor line item. Cost per kilometre: roughly $9 million. Financeable by private syndicates at rational return thresholds. Canada gets a pipeline without a repeat of the TMX fiscal catastrophe.

The TMX Trap Scenario

Jurisdictional challenges fracture the one-review shield. Indigenous consultation litigation extends timelines. Route selection disputes push the proponent submission past 2027. Construction start slides to 2029 or beyond. Capital cost in the range of $38 billion. AFUDC becomes the dominant line item, potentially exceeding 40 percent of total capital expenditure through compounding. Cost per kilometre approaches $34.9 million — the TMX disaster profile. The project becomes un-financeable in private markets and migrates, again, onto the sovereign balance sheet. Canada ends up with two pipelines it cannot sell and a carbon pricing concession it cannot recover.

The gap between these two scenarios is not engineering. It is law, politics, and the speed of institutional decision-making. The entire strategic bet of the Carney-Smith framework is that the regulatory architecture they have announced can hold against the forces that destroyed TMX’s timeline. TMX’s regulatory shield was also considered robust when it was designed. It was not.

V. The Three Hard Gates

Political frameworks do not build pipelines. Capital formation events build pipelines. Between today’s announcement and a first weld, three irreducible gates must be cleared. All three remain open as of the close of May 15, 2026.

Gate One — July 1, 2026: Proponent and Route Submission

Alberta must transition from being the sole applicant in this framework to naming the actual private corporate consortium willing to hold the pen and deploy capital against a locked route. This is not a paperwork exercise. This is the moment at which a corporate board, answerable to shareholders and creditors, must sign its name to a multi-billion-dollar commitment in a regulatory environment that has no precedent for the speed being promised. The question is not whether Ottawa wants a proponent. The question is whether any private syndicate has calculated that the regulatory shield is durable enough to justify the exposure given what they watched happen to TMX. As of May 15, 2026, the answer is publicly unknown. As of May 15, 2026, no hand has gone up.

Gate Two — October 1, 2026: National Interest Designation

The federal Major Projects Office must legally activate the one project, one review protection, creating a demonstrable jurisdictional shield that private capital can underwrite. The first challenge filed against the designation — and one will be filed — will reveal within months whether the framework holds or fractures. Private syndicates will be watching that litigation with the intensity of an options market watching a rate decision. If the shield fractures, the TMX Trap scenario is the operative projection.

Gate Three — September 1, 2027: First Weld

Capital transforms from theoretical corporate liquidity into active field deployment. Steel moves. Welders mobilise. The project becomes a physical fact rather than a political one. Until that date, the entire carbon tax trade-off is a promissory note backed by institutional goodwill and legislative intent — both of which have a well-documented failure rate in Canadian energy infrastructure.

VI. The Accountability Question Both Governments Refused to Answer

A reader asked the question the press conference was architecturally designed to prevent. If the government is not spending money on the pipeline, but has reduced the carbon price trajectory industry would otherwise have paid, and if no private proponent steps forward to build the pipeline — does the taxpayer absorb that cost without receiving the pipeline they were told it would purchase?

The answer is yes. Unambiguously and without a clawback mechanism in the announced framework. The concession is irrevocable. The pipeline is conditional. The carbon price relief has already been granted as of May 15, 2026, regardless of whether a shovel ever enters the ground.

The carbon pricing concession is effective immediately upon the deal’s implementation. The new benchmark schedule — $115 per tonne in 2030, $130 by 2035, $140 by 2040 — is locked into the framework today. It does not require a pipeline to be built in order to take effect. It is the condition of the deal, not the reward for its completion.

The pipeline, by contrast, requires three gates to clear, none of which have been cleared. Each gate can fail independently. The most likely single point of failure is Gate One — the moment at which a private corporate board must sign its name to a multi-billion-dollar construction commitment. The capital community that watched TMX emerge as a stranded sovereign asset will not sign on the assumption that a new regulatory framework has solved what decades of Canadian energy policy failed to solve.

What Smith Got — and When She Got It

Smith received the carbon pricing concession on May 15, 2026. She received it before a route is chosen, before a proponent is named, before a metre of right-of-way is secured, before a single Indigenous consultation obligation has been discharged, and before the Building Canada Act framework has survived its first legal challenge. She received it on the basis of a July 1 deadline for an application that Alberta itself will file as the proponent — because no private proponent exists.

An application is not a pipeline. A government filing its own application to its own regulatory body to initiate a process it has designed to approve itself is not a capital formation event. It is a process designed to preserve the appearance of momentum while the private sector decides whether the regulatory architecture is durable enough to justify commitment. Smith knows this. Carney knows this. The announcement was structured so that the public would not need to know this.

The deal as announced is structurally asymmetric in the industry’s favour. Industry received the carbon pricing concession unconditionally. Government received a promise of a pipeline application by July 1 from a proponent that does not exist. Smith got away with it because no questions were taken. That is this publication’s plain assessment of what happened in Calgary on May 15, 2026.

There is no stated clawback mechanism. If Gate One fails, the carbon pricing trajectory does not revert. The industry retains the lower-cost schedule. The taxpayer has paid the price of a pipeline they did not receive. The climate has absorbed a weaker carbon price signal without the Pathways carbon capture investment that was supposed to accompany it — an investment whose timeline and binding conditions were conspicuously absent from the announced framework despite both governments describing the pipeline and Pathways as mutually dependent.

VII. The AIG Verdict

Mark Carney and Danielle Smith have not built a pipeline. They have constructed a regulatory and fiscal framework that makes pipeline construction theoretically possible at economics private markets might accept — while transferring the risk of failure entirely onto the public balance sheet and granting the industry concession unconditionally.

The instrument deployed is precise in whose interests it serves: trade a $250-billion projected carbon tax liability for a clean regulatory runway, absorb zero sovereign construction risk, and invite the private sector to step onto the tarmac it has just been handed. The tarmac is real. The aircraft remains hypothetical. And the private sector has already demonstrated — by declining to purchase Trans Mountain at par — that a tarmac alone is not sufficient to produce a plane.

AIG governance holds every public institution to the standard of the Socratic question: define what you claim to know. Applied to this announcement, the question produces three answers that remain outstanding as of May 15, 2026.

First: what is the independent, audited estimate of public revenue foregone under the new carbon pricing trajectory — not the industry’s estimate of costs avoided, but the government’s accounting of what public climate investment has been sacrificed to produce this deal?

Second: what is the clawback mechanism if Gate One fails? If no private proponent steps forward by July 1, does the carbon pricing trajectory revert? If not, why not? This question was not asked at the press conference because no questions were taken.

Third: what are the binding conditions on the Pathways carbon capture project? The pipeline and Pathways were described as mutually dependent. The pipeline has three gates and three dates. Pathways has a commitment to continue conversations. These are not equivalent instruments of mutual dependence. The asymmetry is not accidental.

The carbon tax concession is real and irrevocable. Trans Mountain sits unsold on the federal balance sheet. The new pipeline has no private proponent, no route, and no port commitment. Three gates must be cleared. None have been. The governments took no questions. Smith got what she came for on the day of the announcement. The taxpayer is carrying an exposure with no stated recovery mechanism. The Vertical Dispatch will be at Gate One on July 1.

Addendum — The Fourth Gate and the Quiet Expansion Path

A reader surfaced a structural truth that neither government acknowledged and that the public has never been invited to see. It introduces a fourth gate — not regulatory, not political, but economic — and it reframes the entire architecture of the Carney‑Smith announcement.

The oil sands producers now possess a parallel expansion path that is lower‑risk, lower‑cost, and already underway. Optimization of the Enbridge and TMX systems, combined with the proposed South Bow/Bridger corridor, unlocks more than one million barrels per day of new egress capacity without a single weld on the Pacific line. That throughput enables roughly thirty percent production growth without triggering the capital obligations of Pathways and without underwriting a speculative West Coast corridor whose economics remain unproven.

This is the part of the story Canadians were not told: the industry has options. Real ones. Cheaper ones. Faster ones. Options that do not require a $100‑billion capital commitment to fill a pipeline that does not yet exist, and options that do not require binding themselves to a carbon‑capture liability whose terms remain undefined.

The Carney‑Smith framework effectively reduced the future cost of carbon for the oil sands — not through technological innovation, but through political negotiation. The new trajectory replaces a schedule that was politically impossible with one that is slower, lower, and more durable. The concession is real. The obligation it was meant to purchase is not. Industry received certainty. Government received a promise of consideration.

The fourth gate is therefore the capital allocation decision itself: whether the oil sands producers will deploy billions into a high‑risk, high‑cost Pacific corridor when a low‑risk, low‑cost expansion path already exists. Nothing in the announcement compels them to choose the former. Everything in the capital structure incentivises the latter.

The governments built a runway. The industry now has two ways to fly. Only one requires a new plane.

Addendum II — The Ceiling Question: How Far Can the Oil Sands Actually Grow?

A second reader raised the question that sits beneath every projection, every corridor, every emissions model, and every political promise: Is there a limit? Can the oil sands take both expansion paths — the quiet, low‑risk egress now unfolding and the high‑risk Pacific corridor — or does the system itself impose a ceiling?

The answer is structural. The geology is not the limit. The permission structure is.

The oil sands are one of the largest hydrocarbon deposits on Earth. There is no physical barrier to doubling production. The constraints are political, regulatory, capital‑based, and emissions‑based. Canada’s climate commitments, its Section 35 obligations, its carbon pricing regime, its global investor base, and its institutional tolerance for TMX‑scale temporal risk form the real boundary of what the sands can become. The ceiling is not in the rock. It is in the governance.

Industry can pursue both paths — the million‑barrel‑per‑day of low‑risk optimization and, eventually, the Pacific corridor — but only if the political ceiling rises, the emissions architecture stabilises, and capital believes the regulatory shield is durable. None of those conditions exist today. All of them are prerequisites for the second path.

The Pacific corridor is not a geological inevitability. It is a political bet. It requires a private proponent willing to underwrite a multi‑decade liability, a regulatory framework that survives its first constitutional challenge, a global market willing to absorb another million barrels per day, and a federal‑provincial climate architecture capable of reconciling expansion with emissions caps that have not yet been defined. The low‑risk path requires none of these.

The ceiling, therefore, is not the size of the deposit. It is the size of the political and regulatory runway. The sands can grow until one of four constraints binds: the capital ceiling, the regulatory ceiling, the market ceiling, or the political ceiling. The first of those ceilings — capital — is already visible in the industry’s silence on the Pacific corridor.

The geology is infinite. The permission structure is not.

God is Love. Love is Truth. Truth is Consciousness. Consciousness is Brahman

Amen. Namaste.

Dispatch Hashtags

#TheRunwayWithoutAPlane #AIG #VerticalDispatch #TheArchitect #AgeOfConsequences #CarneySmithDeal #TransMountain #TMXUnsold #PipelineAccountability #NoPrivateProponent #CarbonPriceConcession #IrrevocableGiveaway #NoClawback #250Billion #TIERFund #CanadianClimateInstitute #GateOne #GateTwo #GateThree #July1Deadline #BuildingCanadaAct #Section35 #AFUDC #TemporalRisk #PipelineEconomics #SmithGotHers #NoQuestionsAsked #PublicExposure #SubstackCanada #Project2046

There is another gate and that is the decision by the oil sands companies to invest in increased production in order to fill Smith's ephemeral pipeline. Right now, planned optimization of the Enbridge and TMX system and expansion of TMX will add another 600K bpd of capacity fairly quickly. Then there is the South Bow/Bridger pipeline proposal which would add another 450+K bpd. If all go ahead, this 1,050,000+ bpd increase in egress will enable a 30% increase in oil sands production without any commitment to Pathways and that will require capital investment well into the $100 billion+ range. The pipeline to the Pacific addresses the next million bpd but the oil sands companies will be required to commit to spending another big whack of capital now, and put Pathways in place, in order for any private sector entity to agree to build the pipeline. This is a political agreement that is entirely dependent on private capital and there is no indication that the companies are willing to play. Note that in the Oil Sands Alliance press release last week they stated that it was the Premier's goal to double oil production. They did not say that they supported it!